A business is generally entitled for income tax deduction (and GST input tax credits) for the expenditures incurred during the business in order for earning income. There must be nexus between income earning and the expenditure to be deductible in tax purpose, and for certain expenditure, the Commissioner of Taxation does not allow as deductions (e.g. entertainment, fines and meals etc). This is the general rule. So under this rule, you are entitled to claim tax deductions as well as GST credits for what you incur for earning the business income under your business structure.

However, there is a special tax regime called personal services income (PSI) to prevent individuals from reducing their tax by alienating their PSI to an associated company, partnership, trust or individual (sole trader), or by claiming inappropriate “business” deductions.

Where it applies, the PSI regime has the following main effects:

The PSI regime does not apply if:

Although the PSI regime is intended to level the playing field between an employee and a contractor who has PSI, it does not deem contractors to be employees and does not alter the legal relationship between the parties (ITAA97 s.84-10)

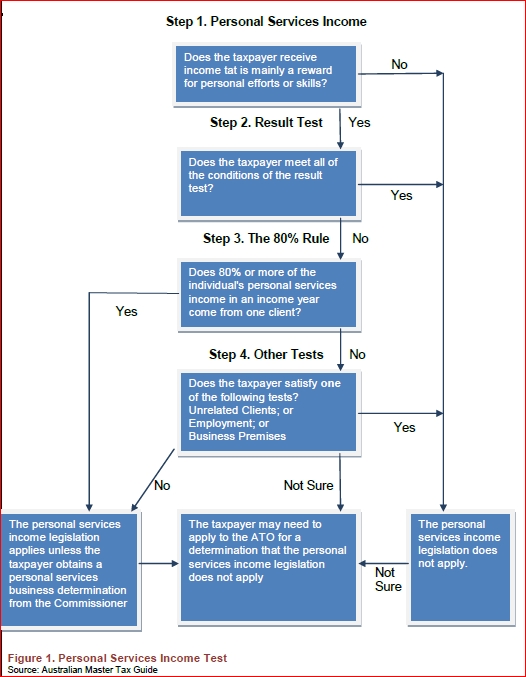

So the matter is:

Whether your income is derived from personal services “BUSINESS” i.e. PSB.

To qualify for the PSB regime, you need to pass tests below.

Result Test

For an individual to satisfy the result test in a particular income year, the individual must satisfy the following three conditions in relation to at least 75% of his or her PSI during the year.

The 80% Rule and Additional Tests

If the result test above is not satisfied, it is necessary to consider the 80% rule.

The unrelated clients test

An individual or personal services entity meets the unrelated clients test in an income year if the service provider gains income from providing services to two or more entities that are not associates or the service provider

The employment test

An individual service provider meets the employment test in an income year if at least 20% of the individual’s principal work for the year is performed by an entity or entities engaged by the individual. The entities cannot be non-individuals that are associates of the individual.

The entity (PSE) meets the employment test where the 20% criterion above is met and the entity or entities engaged are neither:

The business premise test

An individual or a PSE (Service Providing Entity) meets the business premise test in an income year if, at all relevant times during the year, the service provider maintains and uses business premises:

The following diagram shows the tests required to qualify as Personal Services Business (PSB)

{kind=link}

{kind=link}